# Fetching full dataset

import os

import requests

import pandas as pd

import numpy as np

from datetime import datetime

from dateutil.relativedelta import relativedelta

from tqdm import tqdm

import time

PANEL_FILE = "data/crypto_factor/crypto_panel.csv"

FACTOR_FILE = "data/crypto_factor/crypto_factor.csv"

# Skip if data already exists

if os.path.exists(PANEL_FILE) and os.path.exists(FACTOR_FILE):

print(f"Data already exists: {PANEL_FILE}")

print("Skipping fetch. Delete files to re-fetch.")

else:

os.makedirs("data/crypto_factor", exist_ok=True)

BASE_URL = "https://fapi.binance.com"

START_DATE = datetime(2021, 1, 1)

END_DATE = datetime(2025, 11, 1)

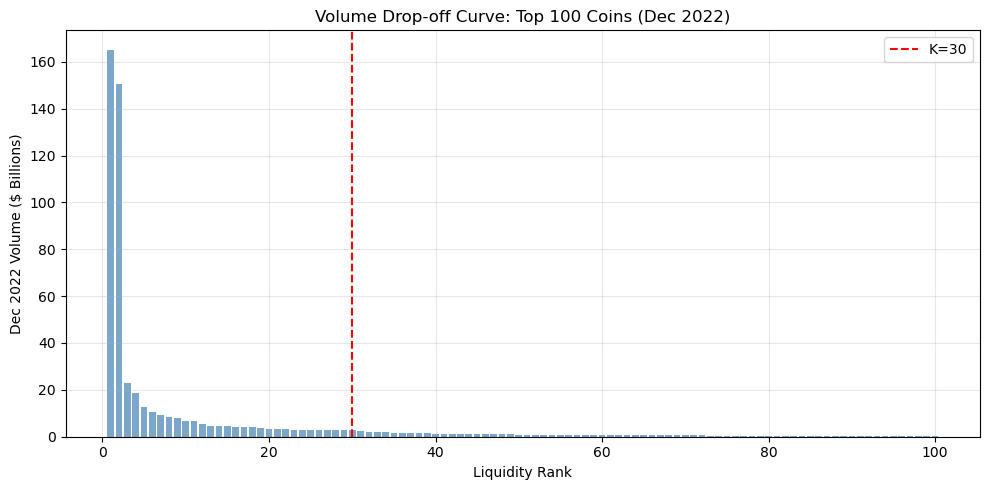

TOP_K = 30

API_DELAY = 0.15

rebal_dates = []

current = START_DATE

while current <= END_DATE:

rebal_dates.append(current)

current += relativedelta(months=1)

print(f"Backtest period: {START_DATE.strftime('%Y-%m')} to {END_DATE.strftime('%Y-%m')}")

print(f"Total months: {len(rebal_dates)}, Universe: Top {TOP_K}")

def get_all_usdt_perpetuals():

resp = requests.get(f"{BASE_URL}/fapi/v1/exchangeInfo")

resp.raise_for_status()

return [s['symbol'] for s in resp.json()['symbols']

if s['symbol'].endswith('USDT') and s['contractType'] == 'PERPETUAL']

def get_monthly_volume(symbol, start_ts, end_ts):

try:

resp = requests.get(f"{BASE_URL}/fapi/v1/klines", params={

"symbol": symbol, "interval": "1M", "startTime": start_ts, "endTime": end_ts, "limit": 1})

data = resp.json()

return float(data[0][7]) if data else None

except: return None

def get_monthly_funding(symbol, start_ts, end_ts):

try:

resp = requests.get(f"{BASE_URL}/fapi/v1/fundingRate", params={

"symbol": symbol, "startTime": start_ts, "endTime": end_ts, "limit": 1000})

data = resp.json()

return np.mean([float(r['fundingRate']) for r in data]) if data else None

except: return None

def get_monthly_return(symbol, start_ts, end_ts):

try:

resp = requests.get(f"{BASE_URL}/fapi/v1/klines", params={

"symbol": symbol, "interval": "1M", "startTime": start_ts, "endTime": end_ts, "limit": 1})

data = resp.json()

if data:

open_p, close_p = float(data[0][1]), float(data[0][4])

return (close_p - open_p) / open_p if open_p > 0 else None

except: pass

return None

def month_to_ts(dt):

return int(dt.timestamp() * 1000)

def get_month_range(dt):

start = datetime(dt.year, dt.month, 1)

end = start + relativedelta(months=1) - relativedelta(seconds=1)

return month_to_ts(start), month_to_ts(end)

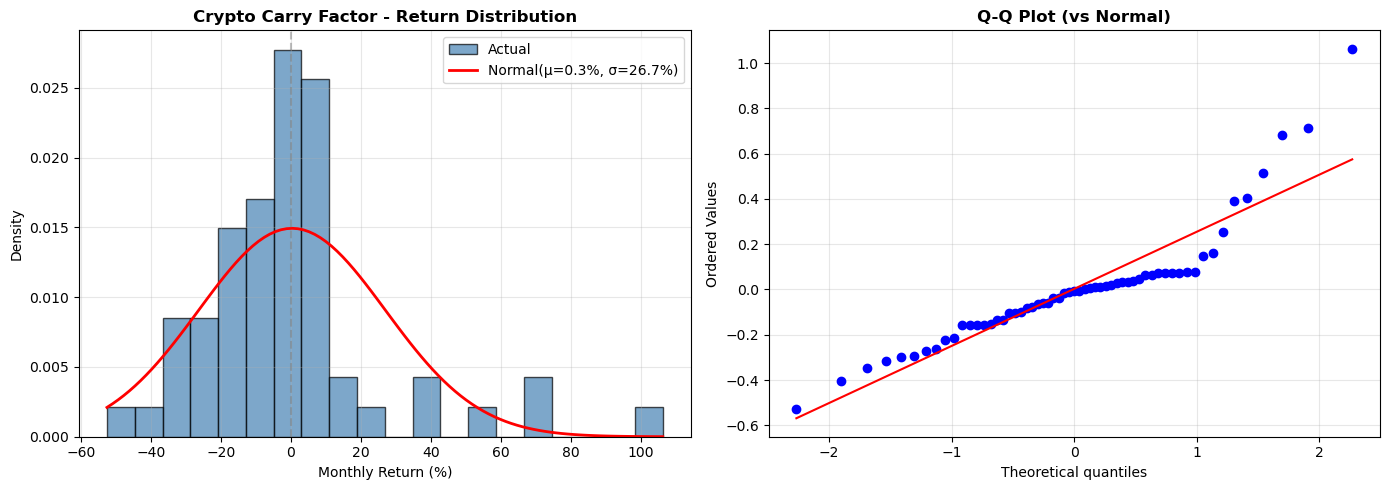

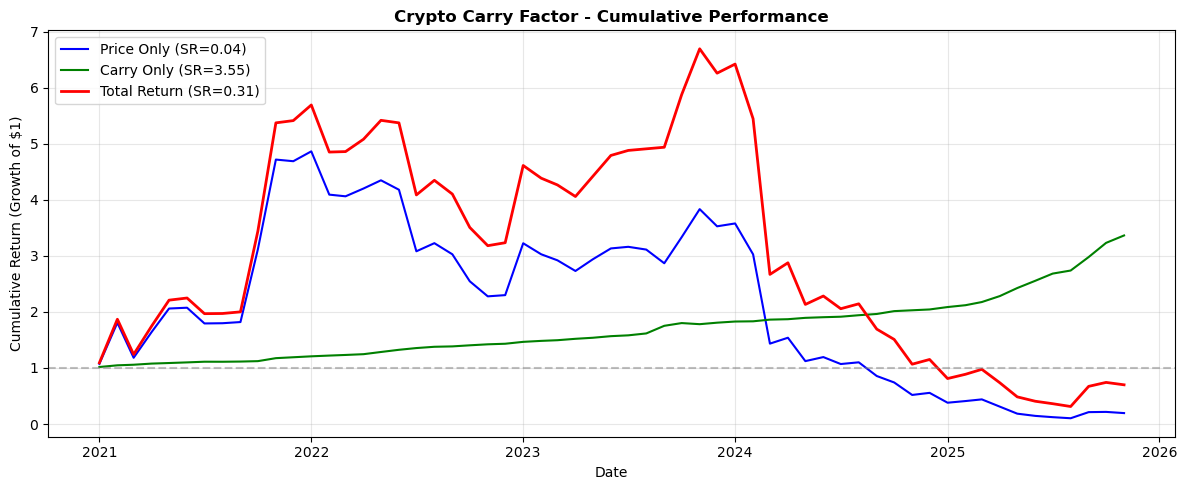

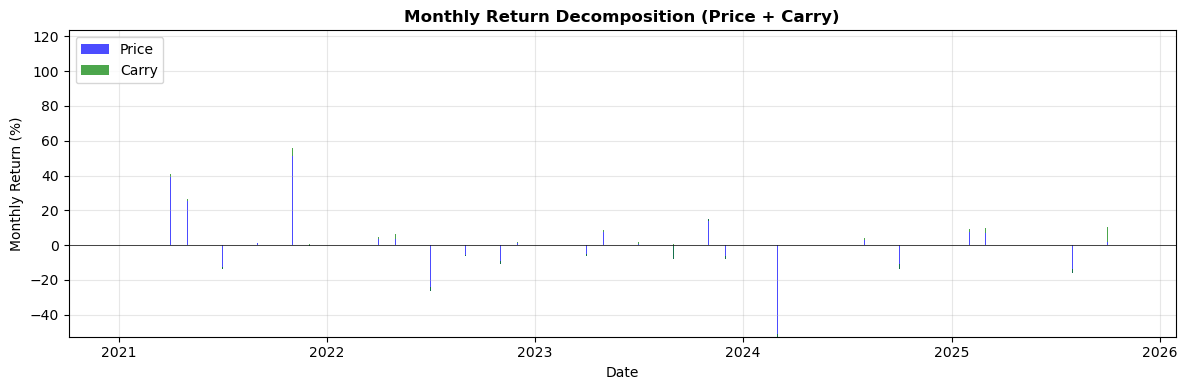

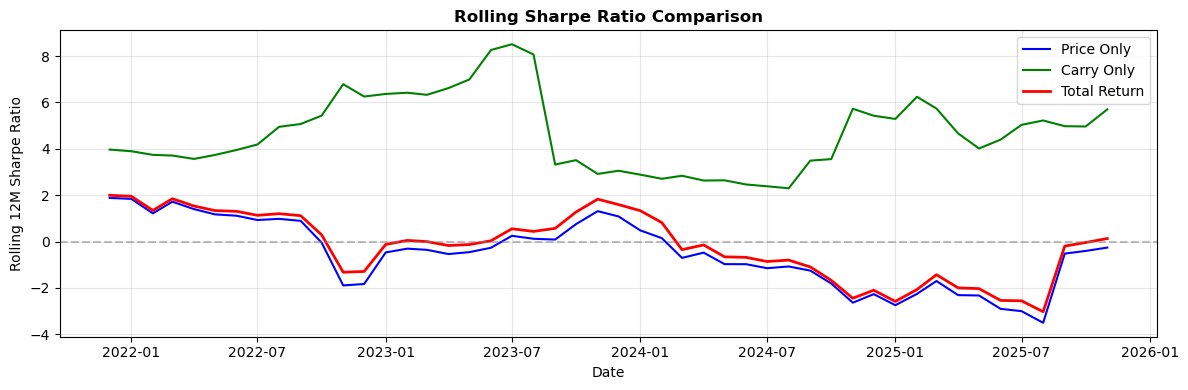

def compute_factor_return(month_panel):

if len(month_panel) < 20:

return None

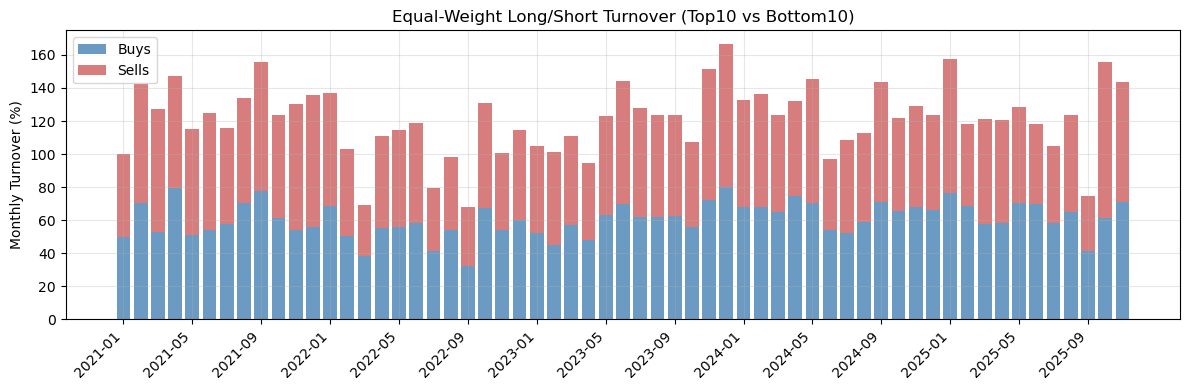

sorted_df = month_panel.sort_values('carry_signal', ascending=False)

long_ret = sorted_df.head(10)['ret_1m'].mean()

short_ret = sorted_df.tail(10)['ret_1m'].mean()

return {'date': month_panel['date'].iloc[0], 'long_ret': long_ret,

'short_ret': short_ret, 'factor_ret': long_ret - short_ret, 'n_assets': len(month_panel)}

# Check existing progress

completed_dates = set()

if os.path.exists(PANEL_FILE):

existing = pd.read_csv(PANEL_FILE, parse_dates=['date'])

completed_dates = set(existing['date'].dt.strftime('%Y-%m-%d'))

print(f"Resuming: {len(completed_dates)} months done")

remaining = [d for d in rebal_dates if d.strftime('%Y-%m-%d') not in completed_dates]

print(f"Remaining: {len(remaining)} months")

if remaining:

all_symbols = get_all_usdt_perpetuals()

print(f"USDT perpetuals: {len(all_symbols)}")

for i, rebal_date in enumerate(remaining):

date_str = rebal_date.strftime('%Y-%m-%d')

print(f"\nProcessing {date_str} ({i+1}/{len(remaining)})")

prior_month = rebal_date - relativedelta(months=1)

prior_start, prior_end = get_month_range(prior_month)

volumes = {}

for sym in tqdm(all_symbols, desc="Volume", leave=False):

vol = get_monthly_volume(sym, prior_start, prior_end)

if vol and vol > 0: volumes[sym] = vol

time.sleep(API_DELAY * 0.3)

universe = sorted(volumes.keys(), key=lambda x: volumes[x], reverse=True)[:TOP_K]

curr_start, curr_end = get_month_range(rebal_date)

records = []

for sym in tqdm(universe, desc="Signals", leave=False):

avg_funding = get_monthly_funding(sym, prior_start, prior_end)

carry_signal = avg_funding * -1 * 3 * 365 if avg_funding else None

ret_1m = get_monthly_return(sym, curr_start, curr_end)

records.append({'date': date_str, 'symbol': sym, 'carry_signal': carry_signal, 'ret_1m': ret_1m})

time.sleep(API_DELAY)

month_panel = pd.DataFrame(records).dropna(subset=['carry_signal', 'ret_1m'])

month_panel.to_csv(PANEL_FILE, mode='a', header=not os.path.exists(PANEL_FILE), index=False)

factor_row = compute_factor_return(month_panel)

if factor_row:

pd.DataFrame([factor_row]).to_csv(FACTOR_FILE, mode='a', header=not os.path.exists(FACTOR_FILE), index=False)

print(f" ✓ {len(month_panel)} rows, factor_ret={factor_row['factor_ret']*100:.2f}%" if factor_row else " ✓ Saved")

print(f"\nComplete: {PANEL_FILE}, {FACTOR_FILE}")